Invoice Factoring Imports

Factoring Invoices To Leverage Import Financing

Invoice factoring imports generates immediate liquidity with no risk and very little cost and no borrowing to finance import transactions

Invoice Factoring Overview

Invoice Factoring is a form of SME finance and common import financing method that involves selling your invoices to professional financiers who are known as a factors. Factors are non-bank alternative source of trade funding who are in the business of purchasing receivables. A factor will pay you the value of your invoices, less a discount for commission and fees.

The factor will advance you most of the invoice amount immediately, and pay you the balance upon receipt of funds from the invoiced party. Transactions close very quickly and you will typically receive funds for newly factored invoices within 48 hours. Factoring provides you with immediate capital based on future income attributable to amounts due on existing invoices. Your invoices function as a record of the credit extended to your customers for which payment is still due.

The terms for invoice factoring transactions vary depending on the amounts, remaining term, credit-worthiness of the customer and the internal policies and practices of the factor. The advance rate, which is the percentage of invoices or accounts receivables which are advanced by the factor vary, along with the discount and factoring fee.

Invoice factoring is not borrowing, no loan is created, no debt is created and you don’t owe money to anyone as a result of factoring your invoices. Factoring transactions do not increase liabilities on your balance sheet. All you do is sell invoices you already own. And there are no restrictions or limitations on how you use the funds you receive from the factor.

See also Accounts Receivable Factoring »

Invoice Factoring Ideas

Factoring invoices provides an ideal financing solution for growing companies in the business of cross-border trade. Invoice factoring delivers immediate liquidity and typically delivered to you within 48 hours. As an import financing idea, you sold all of the goods from your last import transaction and are waiting for payment of the invoices issued for those sales.

Invoice Factoring Idea 1

Rather than waiting until you collect the invoices to undertake your next import deal, factoring your existing invoices will free-up the capital to execute new import transactions sooner. It would shorten the cycle considerably and position you to complete two or three major import transactions annually. Invoice factoring could conceivably increase your income and profit by 20% per year or more.

Invoice Factoring Idea 2

Instead of waiting for payment, factor your invoices and use the extra liquidity to renegotiate more favorable terms and prices with your overseas exporters. The extra cash generated by factoring your invoices would provide you with tremendous leverage when dealing with your foreign vendors. With either idea, Invoice Factoring is the lever that markedly improves your bottom line without borrowing and without incurring risk.

Advantages of Invoice Factoring

No Business Credit Required

Factoring is the sale of invoices or accounts receivable. You are not borrowing money or incurring debt, so you don’t need established business credit for factoring. Factoring credit decisions are based on your customer’s ability to pay, not your business credit. Thus, Invoice Factoring is available to startup companies, when most other financing is not.

Factoring Is Fast

Once you are set up with a factor, you can most often have money in your account in 48 hours or less, much faster turnaround than a bank!

Factoring Is Not Debt

When you factor your invoices, you are selling assets not borrowing money. You do not incur debt of any kind, your liabilities don’t increase, and there is no adverse effect on your balance sheet or other financial statements.

Additional Services

After closing on a factoring transaction, it is not uncommon for the factoring company to provide additional services to their clients such as billing, invoice collections, and account receivable management, saving you time which can be spent on growing your business and increasing sales.

Manage Cash Flow

Invoice Factoring gives you the liquidity you need pay your bills and grow your business. No more waiting 60 days or more to get paid.

Unrestricted Use of Funds

Because factoring is the sale of assets (invoices or accounts receivable), your business is not incurring any debt. Thus there are no restrictions or limitations on the funds you receive from the factor. It’s your money to do with as you please.

Types of Factoring

Traditional Factoring

Traditional factoring is an ideal solution for companies that need extra cash flow to purchase inventory, cover payroll or invest in marketing. You are able to create an immediate influx of cash based on the invoices already on your books. The finance provider, known as the factor purchases all of your accounts receivables and advances you 70% to 90% of the total amount within 24 to 48 hours. The factor pays you the remainder of what you’re owed once your client pays the factor, usually 30 to 45 days later. It deducts a small fee, based on the size and age of each invoice.

Spot Factoring

Small business owners opt for this form of factoring when they do not want to factor all of their invoices. Typically, businesses will want to spot factor when they don’t need a steady flow of cash or have varying gross margins where it does not make sense to factor. Unlike traditional factoring, where the company turns over all invoices, spot factoring is available on an as-needed or one-time basis. This flexibility comes at a premium but often makes sense if you have one client that is particularly slow or if a consistent flow of capital is not needed

Construction Factoring

Construction finance offers sub-contractors and general contractors access to quick cash from your invoices so you can get the funds you need to start your next project. The financier (factor) purchases construction invoices and advances a percentage—often within 24 hours—then collects the funds and forwards the remainder of the invoice to you, less a factoring fee. Few factoring firms work with the construction industry, but we have direct lines into those that do. We will help you find the financial partner that will provide the best solution for your company’s particular situation.

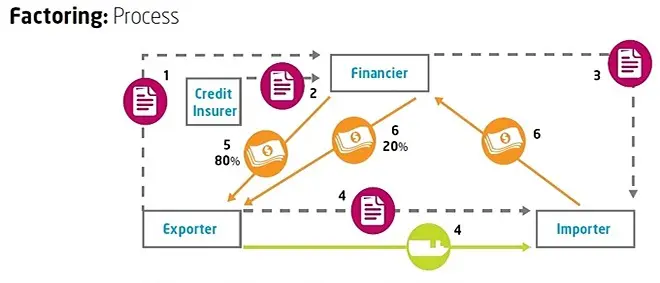

Export Factoring

Export factoring works for companies that want to offer terms to international customers but still want to receive cash when the goods are delivered. The finance company or factor purchases your receivables and forwards payment, usually 70% to 90%, once it has the receivables documentation. The client pays the factor, not you, once it receives the goods. The factor pays you the balance when it receives payment from the customer, less a small fee.

Medical Services Factoring

Medical Services Factoring fills the cash gap inherent with receivables of third-party payers, such as insurance companies, Medicare or Medicaid. It gives you quick access to funds to pay bills, payroll, and buy equipment. With Medical Services Factoring, you perform a service and send the invoice to the factor. The factor then forwards a percentage of the invoice to you. After the factor collects the invoice from the debtor, you receive the remaining amount on the invoice, less the factoring fee.

Recourse v Non-Recourse Factoring

Recourse Factoring is appropriate if you have financially healthy clients. You agree to buy back or exchange with other invoices of equal or greater value, noncollectable invoices. Recourse factoring offers lower fee because of less risk.

With non-recourse factoring risk of insolvency and non-payment is transferred to the Factor. The Factor cannot come back to you for payment if the customer fails to pay. The Factor is not required to cover disputed invoices.

Trade Finance Learning Center

With more than 80% of the world’s trade depending on trade finance it is an essential segment of the financial services sector. It is also one of the least understood of the financial services. One of the things that undermine people’s understanding of trade finance is the absence of a single vocabulary. Do a search for the definition of import financing, for instance, and the top 20 results will provide 20 different definitions. Our trade finance learning center publishes content that we hope will improve understanding of trade finance and its various component segments. Each of the below tabs provides the factual information you need to make good business decisions, beginning with important trade finance definitions.

Accounts Receivable

Accounts Receivable is money owed to a company by a customer for products and /or services sold. Accounts receivable is considered a current asset on a balance sheet once an invoice has been sent to the customer.

Accounts Receivable Factoring

Accounts Receivable Factoring is a method of Trade Financing where a company sells their accounts receivable in exchange for working capital. The purchaser of the receivables relies on the creditworthiness of the customers who owe the invoices, not the subject company.

For details go to Accounts Receivable Factoring »

Advance Against Documents

Advances Against Documents are loans made solely based on the security of the documents covering the shipment.

Asset Based Lending

Asset Based Lending is a method of Trade Financing that allows a business to leverage company assets as collateral for a loan. Asset-based loans are an alternative to more traditional lending which is generally characterized as a higher risk which requires higher interest rates.

Cash Against Documents

Cash Against Documents is the payment for goods in which a commission house or other intermediary transfers title documents to the buyer upon payment in cash.

Cash in Advance

Payment for goods in which the price is paid in full before shipment is made. This method is usually used only for small purchases or when the goods are built to order.

Cash with Order

Cash with Order is the payment for goods whereby the buyer pays when ordering and in which the transaction is binding on both parties.

Commercial Finance

Commercial Finance is defined as the offering of loans to businesses by a bank or other lender. Commercial loans are either secured by business assets, accounts receivable, etc., or unsecured, in which case the lender relies on the borrower’s cash flow to repay the loan.

Confirmed Letter of Credit

A Confirmed Letter of Credit is a Letter of Credit issued by a foreign bank, which has been confirmed as valid by a domestic bank. An exporter whose form of payment is a Confirmed Letter of Credit is assured of payment by the domestic bank who confirmed the Letter of Credit even if the foreign buyer or the foreign bank defaults.

Consignment

Consignment is a delivery of merchandise from an exporter (the consignor) to an agent (the consignee) subject to an agreement by the agent that the agent will sell the merchandise for the benefit of the exporter, subject to certain limitations, like a minimum price. The exporter (consignor) retains ownership of and title to the goods until the agent (consignee) has sold them. Upon the sale of the goods, the agent typically retains a commission and remits the remaining net proceeds to the exporter.

For details go to Consignment Purchase »

Cross-Border Sale

A Cross-Border Sale refers to any sale that is made between a firm in one country and a firm located in a different country.

Factoring

Factoring is the selling of a company’s invoices and accounts receivable at a discount. The lender assumes the credit risk of the debtor and receives the cash when the debtor settles the account.

For details go to Accounts Receivable Factoring »

Invoice Discounting

Invoice Discounting is a type of loan that is drawn against a company’s outstanding invoices but does not require that the company give up administrative control of those invoices.

factoring invoices

factoring invoices is one of the most common methods of trade financing. Your company sells their invoices to a factor in exchange for immediate liquidity. The factor who purchases the invoices relies on the creditworthiness of the customers who owe the invoices, not the subject company.

For details go to factoring invoices »

Irrevocable Letter of Credit

Irrevocable Letter of Credit is a Letter of Credit in which the specified payment is guaranteed by the bank if all terms and conditions are met by the drawee.

Letter of Credit

Letter of Credit or LC is the most common trade finance solution in the world. A Letter of Credit is a document issued by a bank for the benefit of a seller or exporter, which authorizes the seller to draw a specified amount of money, under specified terms, usually the receipt by the issuing bank of certain documents within a given time.

For details go to Letters of Credit For Imports »

Open Account

Open Account is a trade arrangement in which goods are shipped to a foreign buyer without guarantee of payment. The obvious risk this method poses to the supplier makes it essential that the buyer’s integrity be unquestionable.

For details go to Open Accounts »

Pro forma Invoice

Pro forma Invoice is an invoice provided by a supplier prior to the shipment of merchandise, which informs the buyer of the kinds, nature and quantities of goods to be shipped along with their value, and other important specifications such as weight and size.

Receivable Management

Receivable Management involves processing activities related to managing a company’s accounts receivable including collections, credit policies and minimizing any risk that threatens a firm from collecting receivables.

Revocable Letter of Credit

Revocable Letter of Credit is a Letter of Credit that can be canceled or altered by a buyer after it has been issued by the buyer’s bank.

Structured Trade Finance

Structured Trade Finance is cross-border trade finance in emerging markets where the intention is that the loan gets repaid by the liquidation of a flow of commodities.

Trade Credit Insurance

Trade Credit Insurance is a risk management product offered to business entities wishing to protect their balance sheet assets from loss due to credit risks such as protracted default, insolvency, and bankruptcy. Trade Credit Insurance often includes a component of political risk insurance, which ensures the risk of non-payment by foreign buyers due to currency issues, political unrest, expropriation, etc.

Global Report On Business Regulations 2017

Annual Report On Business Regulations Business Regulations that enhance business activity and those that constrain it are examined in World Bank Annual Report On Business Regulations, entitled Doing Business 2017. It is the 14th

IMF Raised 2017 Global Economic Growth Forecast

Global Economic Growth On The Rise Global economic growth is strengthening according to economists at the International Monetary Fund. The IMF sees positive trends in investment, manufacturing, and trade worldwide. As a result, International

World Trade Week Ordered By Trump To Promote Global Trade

World Trade Week Strengthens Economic Growth President Donald Trump has issued a presidential proclamation to create World Trade Week. World Trade Week will take place the week of May 21 through May 27 per

Dublin · Hong Kong · London · Mexico City · Prague · Sydney · Vancouver · Washington DC · Zurich